India's New ECB Framework: What It Actually Means for Mid-Market Lenders

- Mar 25

- 5 min read

Updated: Mar 31

Introduction

The EY Private Credit in India H2 2025 report paints a broadly constructive picture of India's lending landscape. NBFC credit growth accelerated through the second half of 2025. Asset quality improved across most segments. The RBI delivered 125 basis points of cumulative rate cuts during the year, with systemic liquidity returning to surplus. Private credit deal volumes held steady, and domestic fund managers have continued to deepen their presence across the credit spectrum.

Within this picture, however, a structural tension runs through the middle layer NBFC segment. While upper layer entities fund roughly 85% of their borrowings through secured instruments, the figure for middle layer NBFCs sits at approximately 45%. That gap is not incidental. It reflects a different universe of funding channels, and it shows up directly in cost of funds. Credit in this segment is growing, but it is doing so at a structural disadvantage relative to larger peers and against bank lenders who are increasingly competitive in the same secured retail and MSME segments.

One change covered in the EY report deserves specific attention in this context: the overhaul of the External Commercial Borrowing framework. The RBI had released draft amendments in October 2025 that we had discussed previously. After public consultation, the Revised ECB Framework came into force on 16 February 2026 with immediate effect. For the first time, mid-market NBFCs have a regulatory architecture they can realistically work with. Whether the economics support acting on it right now, given where the rupee stands, is a harder question. This article works through both.

Why the ECB Route Was Never Really an Option

The existing ECB framework was not designed with mid-market on-lending NBFCs in mind. 4 features, in combination, made it impractical for this segment:

A restrictive all-in-cost cap. The old ceiling, set at benchmark rate plus 450 to 500 basis points, left little room between what a foreign lender would demand and what the rules permitted for lenders with moderate offshore credit profiles.

MAMP tenors with no relationship to actual loan books. On-lending for working capital or general corporate purposes required a 10-year Minimum Average Maturity Period. On-lending linked to capex-related rupee loan repayment required 7 years. These timelines bore no resemblance to real NBFC portfolios.

On-lending in a regulatory grey area. On-lending as an end-use was not clearly permitted under the framework, creating compliance ambiguity that most legal teams were not willing to accept.

A borrowing cap structured around per-year limits. The US$750 million annual ceiling per entity created rollover complexity without offering the stable, multi-year funding line that liability management actually requires.

The cumulative effect was that most NBFCs in this segment had no practical reason to engage with the ECB route at all.

What the Revised Framework Changes

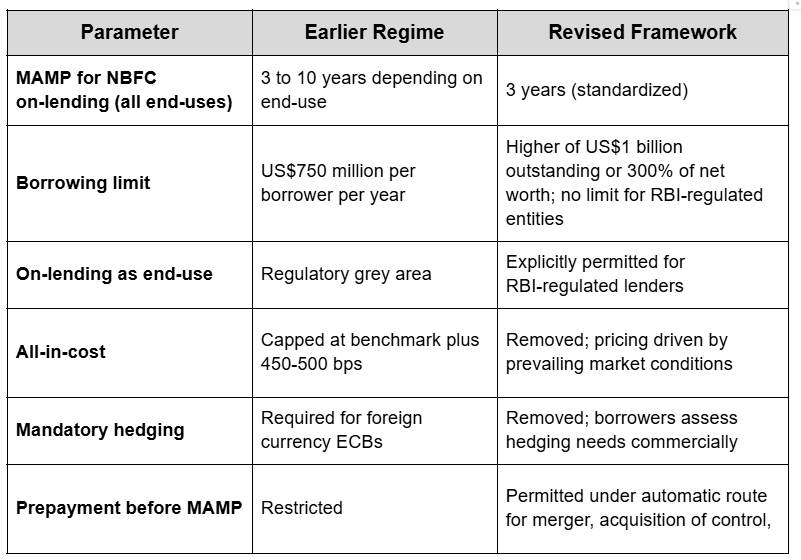

The Revised ECB Framework directly addresses each of these barriers. The table below summarizes the key changes most relevant to this segment:

On the MAMP shift specifically: a standardized 3-year minimum aligns with LAP and equipment finance tenors in a way that requirements of 7 to 10 years never could. For an NBFC with average secured loan tenors of 4 to 6 years, this is the change that converts ECBs from theoretical to practical. The removal of the all-in-cost cap matters equally: AD banks are no longer required to check whether borrowing costs meet a prescribed ceiling, and pricing now reflects the actual credit profile of the borrower.

The Rupee Problem CFOs Are Already Thinking About

The regulatory case for ECBs is now settled. The economic case is harder. Most CFOs in this segment already sense this, and the instinct is correct.

The rupee traded around INR 89.7 to 90.4 per US$ in mid-December 2025 and weakened further to average INR 91.1 per US$ by early 2026. FPI equity outflows in CY2025 reached approximately INR 1.6 trillion. These are not peripheral factors.

The all-in cost of an ECB is not just the foreign currency coupon. It includes the cost of hedging rupee depreciation risk through cross-currency swaps or forward contracts. The revised framework removes mandatory hedging requirements, giving borrowers commercial flexibility. But that flexibility does not eliminate the underlying currency risk. When INR depreciation is expected and demand for rupee hedges is elevated, the hedging cost component rises materially. AA-rated NBFCs have recently issued domestic NCDs at 9% to 10.25% for 15 to 60-month tenors. ECB access creates a cost advantage only if the foreign coupon plus hedging falls meaningfully below that threshold. In the current environment, that arithmetic is strained.

This does not make ECBs irrelevant. It means CFOs should ask not "will ECBs reduce my cost of funds right now" but "under what conditions would they, and am I positioned to act when those conditions arrive."

What to Do Now That the Framework Is Live

The regulations are in force. No supplementary master directions have been issued yet, which means AD banks are working from the revised regulations alone. That creates both urgency and opportunity for lenders who engage early.

Four concrete actions are worth pursuing now:

Map the lending book against the 3-year MAMP. Identify which product segments and loan tenors would actually benefit from ECB funding. LAP, commercial vehicle finance, and equipment lending have natural alignment. Short-tenor MSME working capital does not. This mapping determines whether ECBs are a viable instrument for your institution specifically, not for the sector in general.

Model the all-in cost under multiple rate scenarios. The comparison baseline should be your current marginal cost of domestic NCDs or bank lines. The ECB all-in cost is foreign coupon plus hedging, where hedging is now a commercial decision rather than a regulatory requirement. Model this under current conditions and under a scenario where the rupee stabilizes. This gives you the threshold at which ECBs become economically attractive.

Assess offshore lender readiness. The regulatory framework is open, but offshore lenders will form their own credit view independently. Lenders with audited financials prepared to international standards, established credit ratings, and clean regulatory compliance records will attract interest more readily. Documentation readiness, particularly loan agreement structures that accommodate cross-border lender requirements, is another area where preparation can begin now, regardless of where the rupee trades.

Begin AD Bank conversations now. The all-in-cost ceiling has been removed and AD banks are no longer required to certify market rate compliance. Interpretive practice is forming around the revised regulations without supplementary guidance. Institutions that engage early will help shape that practice rather than inherit conclusions others have reached.

Conclusion

The ECB framework overhaul has removed the barriers that made foreign borrowing largely theoretical for this segment. With MAMP standardized at 3 years, borrowing limits lifted, on-lending explicitly permitted, and the all-in-cost ceiling gone, the regulatory architecture now fits how secured lenders actually operate.

The rupee's depreciation and elevated hedging costs mean most CFOs are right to be cautious about executing right now. That caution is analytically grounded. But caution about timing is different from disengagement. Institutions that exit this period with a clear view of their ECB-eligible loan book, a modelled hedging cost threshold, established AD Bank relationships, and documentation in order will be better placed when conditions shift. Optionality built carefully now costs far less than urgency managed under pressure later.

To know more about OneFin, schedule a Demo.

이용 과정이 간단하고 업무 설명이 명확해서 부담 없이 시작할 수 노래방알바 관련 후기도 많아 참고하기 좋았고 실제 근무 환경도 설명과 비슷해 만족스러운 경험이었습니다.

예약부터 관리 마무리까지 진행이 깔끔하고 서비스 응대도 친절했어요. 이용 중간에 경험한 평택출장마사지 케어는 긴장된 근육을 자연스럽게 풀어줘 정말 만족스러웠습니다.

간편하게 이용 가능한 점이 가장 좋았고 혜택까지 더해져 일상 소비를 조금 더 합리적으로 상품권소액결제 관리할 수 있었습니다.

전체적으로 깔끔하고 효율적인 구조라 만족도가 높았습니다. 서비스는 빠른 처리와 상품권현금화 친절한 안내가 장점이며 반복 이용에도 부담이 없었습니다.

The soft lining and flexible straps help create a gentle wearing experience. bielizna nocna offer balanced support that feels comfortable during travel, work, and everyday movement.